The Rise of Private Credit: Opportunity, Opacity, and Emerging Systemic Risks

Originally published in December 2025, as part of our premium offering for clients.

Background

Publicly traded corporate credit refers to the debt issued by companies and bought and sold on public markets, primarily through corporate bonds and, in some cases, syndicated loans traded on secondary platforms. These instruments allow firms to raise capital for operations, acquisitions, or refinancing, while giving investors access to yield opportunities across varying levels of risk and duration. Corporate credit markets are typically segmented by credit quality — investment grade and high yield — with each segment behaving differently depending on macro conditions, interest rates, and corporate fundamentals.

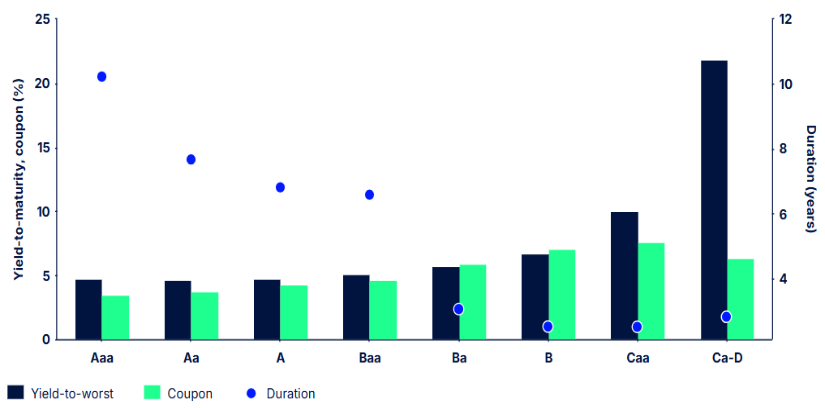

Corporate bonds vary widely in credit quality, from investment-grade issuers with strong balance sheets to high-yield issuers that offer higher returns in exchange for greater risk. Their yields, coupons, and durations fluctuate significantly with economic conditions and credit cycles. Investment-grade corporate credit is generally issued by firms with stronger balance sheets, stable cash flows, and higher credit ratings. These bonds tend to offer lower yields but come with reduced default risk, making them attractive to pension funds, insurers, and other institutions seeking predictable income streams.

High-yield, or “junk,” credit sits on the other end of the spectrum. These issuers carry greater leverage and weaker credit profiles, offering significantly higher yields to compensate investors for elevated risk. High-yield bonds are more sensitive to changes in corporate earnings, liquidity conditions, and market sentiment, and they tend to outperform in periods of economic expansion when default risk is perceived to be low.

Together, the investment-grade and high-yield markets form the backbone of public corporate financing, shaping how companies access capital and how investors manage risk and return across cycles. Corporate credit plays a central role in the real economy because firms’ borrowing costs and access to capital directly influence hiring, investment, and strategic decisions.

Shifts in credit conditions can amplify or dampen economic slowdowns, and the balance between bank loans and bonds affects how monetary policy is transmitted. For example, when bond markets tighten and yields spike, firms dependent on public issuance may face immediate refinancing pressure. In contrast, firms with strong banking relationships may experience more stable funding conditions. Understanding how and where firms borrow is therefore essential for assessing financial stability, corporate vulnerability, and macroeconomic outcomes.

Private credit, on the other hand, involves non-bank lenders providing customized loans directly to companies — often mid-market firms that can’t easily tap banks or public markets. These deals are illiquid, negotiated privately, and far less transparent, but they offer higher yields to compensate for greater risk and limited disclosure. For investors, private credit’s main strengths are enhanced returns, diversification, and the ability to shape terms to fit specific risk-return preferences.

Borrowers benefit from more flexible structures, speed, confidentiality, and bespoke financing that public markets cannot provide. Public credit’s advantages include ease of trading, rich market transparency, lower costs of capital for high-quality issuers, and access to a broad investor base. Each market serves different needs: private credit for tailored, higher-risk, higher-return financing; public credit for standardized, liquid, and lower-risk borrowing.

Current Trends

The corporate credit market has grown substantially over the past few decades, shaped by macroeconomic cycles, financial innovation, regulatory changes, and shifts in investor demand. The proliferation of bond issuance — particularly after the Global Financial Crisis — was supported by low interest rates, strong appetite for yield, and the development of deep secondary markets.

U.S. firms borrow across multiple credit markets, and conditions in these markets don’t always move together. Over the past two decades, bond market conditions have often diverged from bank lending standards, reacting more quickly to changes in economic outlook and monetary policy. As a result, the credit cycle for firms borrowing through loans can differ from that of firms relying on public debt markets.

Data from Capital IQ showed that the share of bank-intermediated credit has risen on average, but this trend is driven by more firms borrowing exclusively from banks. Among firms with access to both loans and bonds, reliance on bank credit has actually fallen — especially for smaller firms in the bottom 75th percentile of the size distribution, which increasingly favor bond financing. Meanwhile, firms with access to both markets can shift between bonds and loans depending on cyclical conditions.

At the same time, corporate bond maturities have shortened significantly, falling from about eleven years in 2002 to under 8.5 years in 2022, while loan maturities have also declined since the financial crisis. This means firms must refinance more often, making them more sensitive to conditions in the corporate bond market. Overall, shifts in debt composition and maturity structure shape not only firm-level financing flexibility but also the transmission of monetary policy and broader macroeconomic dynamics.

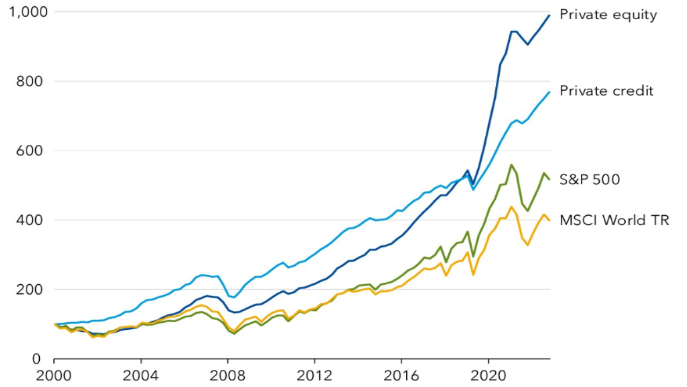

The private credit market has grown rapidly to more than $2.1 trillion globally in 2024, becoming a major financing source for mid-sized and riskier companies that sit between traditional bank lending and public bond markets. Its appeal comes from speed, flexibility, and higher yields, attracting institutional investors such as pension funds and insurers.

But this shift of lending activity from regulated, transparent markets into a more opaque ecosystem has introduced new vulnerabilities, including infrequent valuation, weaker underwriting standards, and rising borrower stress as interest costs exceed earnings for a growing share of firms.

The market’s rapid expansion, hidden leverage, and complex interconnections raise concerns about how shocks could spread. Many private credit borrowers are smaller and more highly leveraged, private loans are marked infrequently and may mask losses, and pressure to deploy capital has weakened loan covenants. Data gaps also make it difficult to assess how risks flow across private credit funds, private equity firms, banks, insurers, and increasingly retail-focused vehicles that may face higher redemption risks under stress.

First Brands, a major car-parts supplier built through years of debt-fueled acquisitions, filed for bankruptcy in September 2025 after relying heavily on opaque off-balance-sheet financing. The company had used private debt markets and invoice factoring to mask the true scale of its liabilities—estimated between $10bn and $50bn—raising concerns about missing funds and whether invoices were pledged multiple times. Its sudden implosion has unsettled investors not because of the business itself, but because of how little is known about the private debt structures underlying it.

The failure has intensified fears that First Brands may signal deeper weaknesses in the rapidly expanding private debt market. Similar issues surfaced with the recent collapse of Tricolor, a subprime auto lender, suggesting broader stress in parts of the auto ecosystem as consumers face economic pressure. Experts warn that private credit markets lack the transparency of public markets, making it difficult to track where risky assets are held and increasing the danger of hidden losses spreading through financial institutions.

Wall Street’s worry is that First Brands could be the first domino in a chain of failures tied to undisclosed leverage and unregulated financing structures. With parallels drawn to past crises—from Greensill to Lehman—economists caution that impaired assets sitting in opaque funds could create unexpected contagion risks. If additional failures emerge, the shock could ripple through banks, asset managers, and credit markets, revealing systemic vulnerabilities that have been building below the surface.

JPMorgan wrote off $170 million tied to Tricolor, with CEO Jamie Dimon acknowledging the bank’s oversight failures and calling the episode “not our finest moment.” He warned that after more than a decade of a credit bull market, these bankruptcies may be early indicators of excesses building in the system. As Dimon put it: “When you see one cockroach, there are probably more,” underscoring fears that hidden pockets of risk may surface if economic conditions weaken.

Executives at Citigroup, Wells Fargo, and BlackRock emphasized on post-earnings calls that overall borrower credit quality remains strong and that the Tricolor and First Brands cases appear idiosyncratic rather than systemic. Even so, several institutions—including Jefferies and UBS—have disclosed limited exposure to First Brands, and BlackRock has taken steps to redeem money from a Jefferies-managed fund connected to the company’s debt.

Despite the turmoil, many large banks and investment firms maintain that the broader corporate and consumer credit markets remain healthy, pointing to declining default rates in the syndicated loan space and stable performance across most borrowers. BlackRock’s CFO noted that recent bankruptcies are concentrated in syndicated and CLO markets, not in the core portfolios of major private credit managers.

Goldman Sachs and Citigroup echoed this sentiment, highlighting robust underwriting standards, active monitoring, and limited exposure to the troubled names. Still, the sudden failures of First Brands and Tricolor have prompted a period of soul-searching on Wall Street, reinforcing that even in a strong credit environment, weaknesses can lurk in specialized sectors—and that rigorous risk controls remain essential as the credit cycle matures.

Policymakers argue that stronger oversight is needed to prevent these vulnerabilities from becoming systemic. Priorities include enhanced monitoring of leverage and interconnectedness, better data and reporting standards, closer coordination among regulators, and greater attention to liquidity management — especially for retail-access products. Without such measures, a downturn could expose hidden losses, trigger funding strains, and constrain lending to companies, amplifying economic stress.

Academic Research

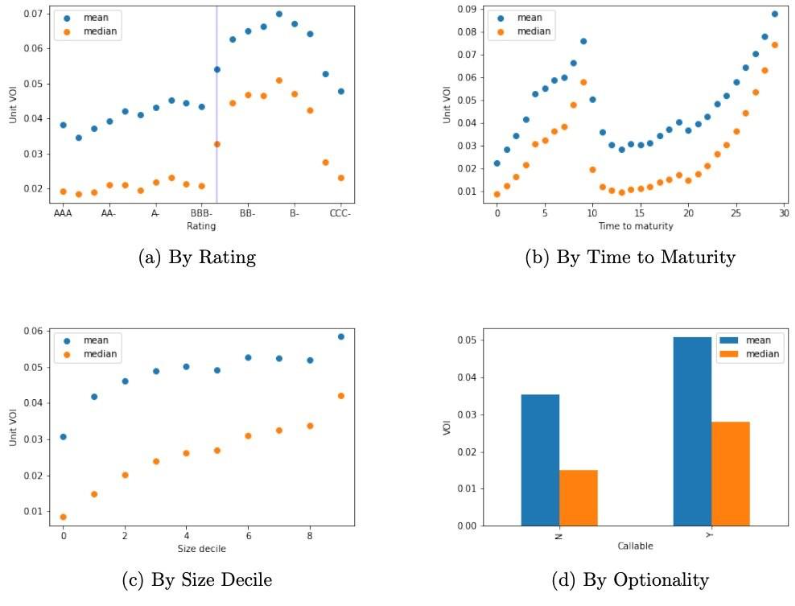

Academic researchers have argued that certain datasets are more valuable to fixed income investors than others. Bai et al. (2023) estimated the value of data according to its usefulness for prediction and potential gains from prediction. They found that information about high-yield bonds is more valuable than investment-grade bonds as they are more likely to default. The value of data was also found to rise with time to maturity but experienced a sharp fall at the ten-year mark. Empirical findings also pointed to the value of information increases with bond liquidity as measured by transitory price movements.

Avalos et al. (2025) studied the growth and drivers of private credit, noting its prominence in countries with lower policy rates, stricter banking regulations, and less efficient banking sectors. In the U.S., the cost of capital for business development companies (BDCs) has declined over the past decade, narrowing banks’ initial funding advantage and reshaping the relationship between banks and private credit.

Private credit can complement traditional banking by providing stability benefits, as its closed-end structure and matched maturities make it better suited for long-term loans. Its specialization in niche markets also offers informational advantages, flexible loan terms, and enhanced risk screening and monitoring, which borrowers value.

However, the advantages of private credit may diminish as the asset class evolves. Growing participation from retail investors through open-ended structures could create liquidity mismatches, making private credit vulnerable to similar risks as banks. The end of persistently low interest rates may reverse BDCs’ funding cost advantage, and increased diversification to appeal to broader investors could dilute funds’ local expertise.

From a financial stability perspective, changes in investor composition, leverage, and portfolio concentration, combined with deeper interlinkages between banks and private credit funds, warrant careful monitoring to assess potential systemic implications.

Alternative Datasets for Corporate and Private Credit

Alternative datasets for corporate and private credit are increasingly used for a more detailed and real-time understanding of a borrower’s financial health and risk profile. These datasets draw from a variety of sources, including SEC filings, Federal Reserve APIs, stock exchange APIs, and web scraped data allowing investors to aggregate financial disclosures, market activity, and corporate filings quickly.

Eagle Alpha’s F.A.I.L (Forecast Analysis Insolvency Likelihood) dataset provides a forward-looking view of U.S. bankruptcy trends by capturing roughly 85% of all business and consumer filings and analyzing how these processes are initiated. Updated weekly, it produces sector- and state-level forecasts with a 16-week lead time and approximately 97% predictive accuracy. By combining software-captured initiation data with public information, the dataset offers granular NAICS-mapped insights, early warning indicators of financial stress, and macro-level signals that help investors assess sector resilience, value-chain risk, and distressed or turnaround opportunities.

Cardinal Analytics’ Default Risk Monitor (DRM), for example, uses machine learning to identify companies at high risk of default, supporting research, screening, and validation of credit events in both credit and equity markets. The tool delivers daily end-of-day scores ranging from 0 to 1, offering timely warnings before defaults are reflected in bond prices. DRM covers approximately 1,000 North American rated companies and around 3,000 globally rated companies, and it has demonstrated significantly higher predictive accuracy than traditional credit risk models.

SOLVE, on the other hand, provides data and analytics solutions for the fixed income market, with a focus on the traditionally opaque private credit sector. Its Private Credit Data and Analytics platform aggregates and standardizes information from 162 BDCs, covering over 46,000 investments across roughly 10,000 portfolio companies and more than $475 billion in AUM, offering users comprehensive market visibility and actionable insights. The platform serves institutional investors, analysts, traders, law firms, and asset managers, enabling confident, data-driven decision-making and improving transparency in private markets.

Want to explore how credit data fits into your investment workflows? Contact the Eagle Alpha team to learn more about our data sourcing and research solutions.